All Categories

Featured

Table of Contents

For many people, the largest problem with the boundless financial concept is that initial hit to early liquidity created by the costs. This con of limitless banking can be minimized significantly with correct plan style, the very first years will certainly constantly be the worst years with any type of Whole Life policy.

That stated, there are certain limitless financial life insurance coverage plans created mainly for high early money value (HECV) of over 90% in the very first year. The lasting performance will certainly frequently considerably delay the best-performing Infinite Banking life insurance policy plans. Having accessibility to that additional 4 figures in the initial few years might come with the expense of 6-figures down the road.

You actually get some considerable long-term benefits that help you recover these early costs and afterwards some. We locate that this prevented early liquidity problem with boundless banking is a lot more psychological than anything else once extensively discovered. As a matter of fact, if they definitely needed every dime of the money missing from their infinite financial life insurance policy plan in the initial few years.

Tag: unlimited banking idea In this episode, I discuss finances with Mary Jo Irmen who shows the Infinite Financial Concept. This subject may be controversial, but I intend to obtain varied views on the program and learn more about different approaches for farm financial management. Some of you might concur and others will not, however Mary Jo brings an actually... With the surge of TikTok as an information-sharing platform, monetary advice and strategies have found an unique way of dispersing. One such technique that has been making the rounds is the infinite financial idea, or IBC for short, amassing endorsements from stars like rapper Waka Flocka Flame. While the technique is currently popular, its roots map back to the 1980s when financial expert Nelson Nash introduced it to the globe.

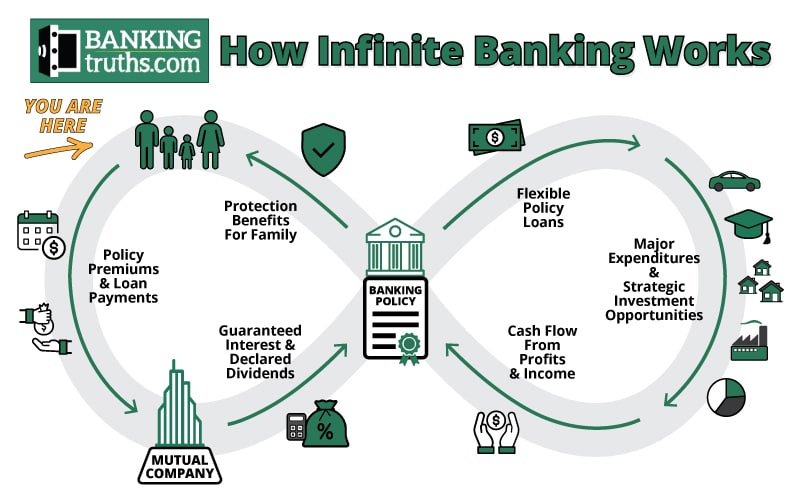

Within these policies, the cash worth grows based upon a price set by the insurance company. When a substantial cash value gathers, insurance policy holders can get a money worth lending. These fundings vary from traditional ones, with life insurance policy acting as collateral, suggesting one could lose their insurance coverage if borrowing exceedingly without sufficient cash value to sustain the insurance prices.

And while the attraction of these plans is noticeable, there are natural limitations and dangers, demanding persistent cash worth surveillance. The approach's legitimacy isn't black and white. For high-net-worth individuals or local business owner, specifically those using approaches like company-owned life insurance policy (COLI), the benefits of tax breaks and compound development can be appealing.

Nelson Nash Institute

The allure of boundless banking does not negate its obstacles: Cost: The fundamental need, an irreversible life insurance plan, is more expensive than its term counterparts. Eligibility: Not every person qualifies for entire life insurance policy due to extensive underwriting processes that can exclude those with specific wellness or way of life conditions. Intricacy and danger: The intricate nature of IBC, paired with its dangers, might discourage lots of, particularly when easier and much less dangerous choices are offered.

Designating around 10% of your regular monthly income to the plan is simply not practical for many individuals. Part of what you check out below is simply a reiteration of what has actually already been said over.

So prior to you get on your own right into a circumstance you're not planned for, know the following first: Although the principle is frequently sold because of this, you're not really taking a funding from on your own. If that were the situation, you would not have to repay it. Instead, you're obtaining from the insurance provider and have to repay it with passion.

Some social media articles recommend utilizing money value from entire life insurance policy to pay for credit history card financial debt. The concept is that when you settle the funding with passion, the amount will certainly be sent back to your financial investments. Unfortunately, that's not just how it functions. When you pay back the car loan, a section of that passion goes to the insurer.

For the initial a number of years, you'll be repaying the payment. This makes it incredibly difficult for your plan to collect value throughout this moment. Entire life insurance policy prices 5 to 15 times more than term insurance coverage. Most individuals just can not manage it. Unless you can afford to pay a couple of to a number of hundred bucks for the next years or even more, IBC won't function for you.

Start Your Own Bank Free

Not everybody should count entirely on themselves for monetary security. If you call for life insurance coverage, below are some beneficial ideas to think about: Consider term life insurance coverage. These policies supply insurance coverage throughout years with significant monetary commitments, like home loans, student finances, or when caring for little ones. Make certain to look around for the very best price.

Copyright (c) 2023, Intercom, Inc. () with Reserved Typeface Call "Montserrat". This Typeface Software application is licensed under the SIL Open Up Typeface Permit, Version 1.1. Copyright (c) 2023, Intercom, Inc. (legal@intercom.io) with Scheduled Typeface Name "Montserrat". This Font style Software program is accredited under the SIL Open Typeface License, Variation 1.1.Skip to primary content

Visa Infinite Alliance Bank

As a CPA focusing on actual estate investing, I have actually combed shoulders with the "Infinite Financial Idea" (IBC) a lot more times than I can count. I've even spoken with professionals on the subject. The main draw, aside from the noticeable life insurance coverage advantages, was constantly the idea of accumulating money worth within an irreversible life insurance policy plan and borrowing against it.

Certain, that makes feeling. Honestly, I constantly believed that cash would certainly be better spent straight on financial investments instead than funneling it via a life insurance coverage policy Up until I uncovered just how IBC might be integrated with an Irrevocable Life Insurance Coverage Trust Fund (ILIT) to produce generational wealth. Let's begin with the basics.

Infinitive Power Bank

When you obtain against your policy's money value, there's no collection payment routine, giving you the liberty to handle the car loan on your terms. The cash money value proceeds to grow based on the policy's guarantees and dividends. This arrangement allows you to gain access to liquidity without interrupting the long-lasting development of your plan, provided that the lending and passion are managed sensibly.

The process continues with future generations. As grandchildren are born and expand up, the ILIT can purchase life insurance plans on their lives. The trust after that collects several plans, each with growing cash worths and survivor benefit. With these policies in position, the ILIT properly comes to be a "Family members Bank." Member of the family can take car loans from the ILIT, utilizing the money worth of the policies to fund investments, begin services, or cover major expenses.

An important element of managing this Household Financial institution is using the HEMS criterion, which stands for "Health, Education And Learning, Maintenance, or Assistance." This guideline is usually included in trust arrangements to direct the trustee on just how they can distribute funds to recipients. By adhering to the HEMS standard, the depend on ensures that distributions are created vital demands and lasting support, protecting the depend on's possessions while still offering for relative.

Increased Versatility: Unlike inflexible small business loan, you manage the repayment terms when borrowing from your very own plan. This permits you to structure repayments in a method that lines up with your company cash money flow. whole life insurance infinite banking. Enhanced Cash Flow: By funding overhead with policy financings, you can possibly liberate money that would certainly otherwise be locked up in typical funding settlements or tools leases

He has the same devices, but has likewise constructed added cash money worth in his policy and got tax advantages. Plus, he now has $50,000 readily available in his policy to use for future opportunities or expenditures. Regardless of its prospective advantages, some individuals remain skeptical of the Infinite Banking Concept. Let's deal with a couple of typical worries: "Isn't this simply expensive life insurance policy?" While it's real that the premiums for a correctly structured entire life policy might be greater than term insurance policy, it is essential to view it as even more than simply life insurance.

Nelson Nash Life Insurance

It's regarding developing a versatile funding system that gives you control and supplies numerous advantages. When made use of strategically, it can enhance various other investments and organization methods. If you're intrigued by the capacity of the Infinite Banking Idea for your organization, here are some steps to take into consideration: Educate Yourself: Dive deeper right into the principle through reliable publications, seminars, or assessments with knowledgeable specialists.

{kind=link}

Table of Contents

Latest Posts

Bank On Yourself Review Feedback

Nelson Nash Institute

Infinite Banking Solution

More

Latest Posts

Bank On Yourself Review Feedback

Nelson Nash Institute

Infinite Banking Solution